Predictive Cash Flow Technology:

How Smart Businesses See Money Problems Before They Happen

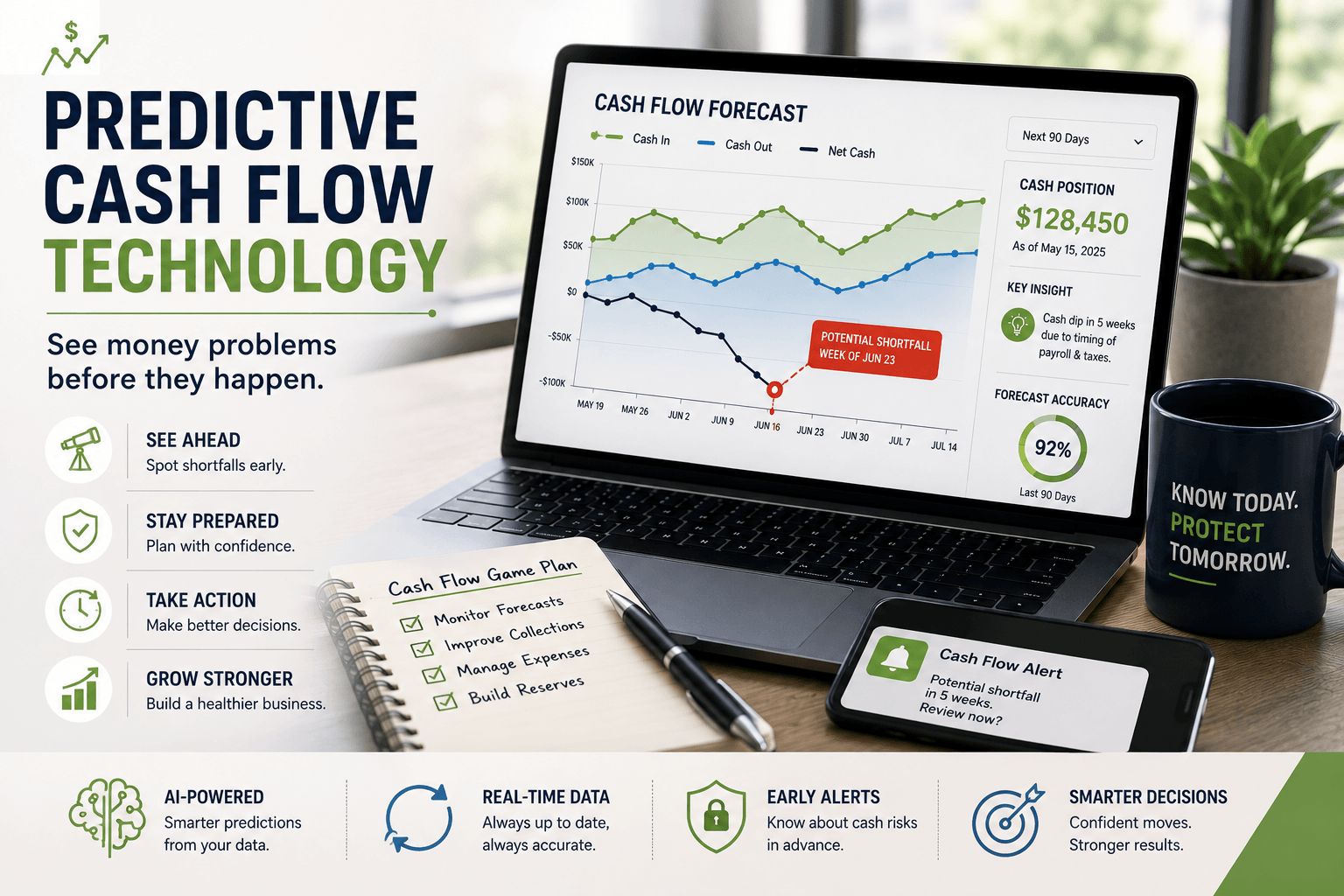

Predictive cash flow technology uses AI, machine learning, and real-time financial data to forecast your future cash position—so you can spot shortfalls, time payments, and make confident decisions weeks or months before your bank balance forces your hand.

Here’s what I’ve learned after two decades helping thousands of small businesses manage their books: most companies don’t fail because they’re unprofitable. They fail because they run out of cash at the wrong moment. And the heartbreaking part? Nearly every one of those crises was visible in the data—weeks in advance. The tools to see it coming finally exist, and they’re no longer reserved for Fortune 500 finance teams. Let me show you how this works and why it changes everything.

What is predictive cash flow technology and how does it work?

- Predictive cash flow technology combines AI analytics, historical financial data, and real-time inputs to forecast future cash positions automatically and accurately.

- It pulls data from your accounting system, bank feeds, AR, and AP to build a living forecast that updates continuously.

- Machine learning models detect patterns—like which customers pay late—that static spreadsheets simply miss.

- It flags future shortfalls early, giving you time to act instead of react.

- Clean, current bookkeeping is the fuel; without accurate records, even the smartest model produces unreliable forecasts.

Why Traditional Cash Flow Forecasting Falls Short

Let’s be honest about the old way: a spreadsheet, updated monthly (maybe), built on guesses about when invoices will actually get paid. By the time you finish it, it’s already outdated.

Traditional cash flow forecasting is still essential—the U.S. Small Business Administration lists it among the core disciplines of managing your finances. But manual forecasting has three fatal flaws: it’s slow, it’s static, and it’s only as good as your assumptions. A 2022 U.S. Bank–cited analysis famously found that 82% of small business failures involve poor cash flow management. That’s not a profitability problem. That’s a visibility problem.

Predictive tools solve this by replacing assumptions with pattern recognition. Instead of guessing that Customer A pays in 30 days, the model knows they average 47.

How AI Cash Flow Analytics Transforms Liquidity Planning

This is where predictive cash flow technology earns its keep. When your forecast updates daily instead of monthly, you stop discovering problems—you start anticipating them.

Strong liquidity forecasting means knowing not just how much cash you’ll have, but when you’ll have it. A predictive system might show you that despite a strong quarter ahead, week six holds a dangerous dip because payroll, a tax payment, and a slow-paying client all collide. Now you have six weeks to arrange a line of credit, accelerate collections, or delay a purchase—on your terms.

The real-time visibility advantage

The Federal Reserve’s Small Business Credit Survey consistently shows that uneven cash flow is one of the top financial challenges small firms face. Businesses with real-time cash flow visibility negotiate financing from a position of strength rather than desperation. Lenders notice the difference—and so does your stress level.

The best forecasts start with accurate books. Let Complete Controller help you build a stronger financial future.

Using Predictive Tools to Improve Working Capital Decisions

Forecasting is only half the game. The real win is acting on what the forecast tells you. Predictive insights sharpen every working capital lever you have:

- AR timing: Identify which invoices are statistically likely to go late—and follow up before they do.

- AP strategy: Pay vendors on the optimal date, capturing early-pay discounts without starving your cash reserves.

- Inventory decisions: Time large purchases around predicted cash peaks instead of gut feel.

- Cash conversion cycle: Shorten the gap between spending money and collecting it.

That last point deserves emphasis. True cash management optimization means compressing the days between outflow and inflow—and predictive analytics shows you exactly where the cycle is leaking. Research from PwC has estimated that companies globally leave over €1.2 trillion trapped in working capital. For a small business, freeing even a fraction of that is transformational.

Clean Books: The Foundation Every Prediction Depends On

Here’s the truth nobody selling software wants to say out loud: predictive technology cannot fix messy bookkeeping. Garbage in, garbage forecast out.

Your model is learning from your historical data. If invoices are entered late, expenses are miscategorized, or bank reconciliations lag by weeks, the AI learns from fiction. This is why I tell every client that reliable automated cash flow forecasting for SMBs starts with disciplined, current, accurate books. At Complete Controller, we’ve watched forecast accuracy jump dramatically the moment a client’s records get cleaned up and kept current in the cloud.

What quality data looks like

Daily bank feeds reconciled weekly. AR and AP entered as they happen, not at month-end. Consistent categorization. It’s not glamorous—but it’s the difference between a forecast you trust and one you ignore.

Adopting AI Responsibly: Governance Still Matters

I’m bullish on this technology, but I’m not naive about it. AI models can drift, embed bias, or produce confident-sounding nonsense. That’s why frameworks like the NIST AI Risk Management Framework exist—to help organizations use AI-driven cash flow forecasting tools with appropriate oversight.

The practical version for your business is simple:

- Validate the forecast against actual results monthly and track accuracy.

- Keep a human in the loop—AI informs decisions; it doesn’t make them.

- Understand the inputs so you know when a forecast might be skewed.

- Review model assumptions whenever your business changes significantly.

Technology amplifies judgment. It doesn’t replace it.

Getting Started with Predictive Cash Flow Technology

You don’t need an enterprise budget. Start where you are: get your books clean and current, connect a forecasting tool to your accounting platform, and run predictions alongside your existing process for 60–90 days. Once you see the accuracy, you’ll never go back to spreadsheet guesswork.

The businesses that thrive in the next decade won’t be the ones with the most cash—they’ll be the ones who can see their cash the furthest ahead.

Conclusion

Predictive cash flow technology turns cash management from a rearview mirror into a windshield. It replaces stale spreadsheets with living forecasts, exposes shortfalls before they become emergencies, and gives you the confidence to make bold decisions with clear eyes. But remember: the smartest AI in the world is only as good as the books beneath it.

That’s where we come in. My team at Complete Controller pioneered cloud-based bookkeeping and controller services, and we’ve helped thousands of businesses build the clean, current financial foundation that makes predictive forecasting actually work. Ready to see your cash future clearly? Visit Complete Controller and let’s build it together.

Frequently Asked Questions About Predictive Cash Flow Technology

What is predictive cash flow technology?

It’s software that uses AI and machine learning to analyze your historical and real-time financial data—bank feeds, AR, AP, and accounting records—to forecast your future cash position automatically.

How accurate is AI cash flow forecasting?

Accuracy depends heavily on data quality. With clean, current bookkeeping, predictive models routinely outperform manual spreadsheets because they learn actual payment patterns rather than relying on assumptions.

Is predictive cash flow software worth it for small businesses?

Yes. Since most small business failures involve cash flow problems, early visibility into shortfalls delivers outsized value—often preventing crises that would cost far more than the software.

What data do predictive cash flow tools need?

They typically need connected bank accounts, accounts receivable and payable records, historical transactions from your accounting system, and consistent categorization to detect reliable patterns.

Can predictive forecasting replace my bookkeeper or accountant?

No—it depends on them. Predictive models learn from your books, so accurate, timely bookkeeping is the foundation. Human financial expertise interprets the forecast and makes the final call.

Sources

- Complete Controller. Liquidity: Key to SME Success. https://www.completecontroller.com/liquidity-key-to-sme-success/

- Complete Controller. Mastering the Cash Conversion Cycle. https://www.completecontroller.com/mastering-the-cash-conversion-cycle/

- Complete Controller. Small Business Bookkeeping: 9 Tips and Tricks. https://www.completecontroller.com/small-business-bookkeeping-9-tips-and-tricks/

- U.S. Small Business Administration. Manage Your Finances. https://www.sba.gov/business-guide/manage-your-business/manage-your-finances

- National Institute of Standards and Technology (NIST). AI Risk Management Framework. https://www.nist.gov/itl/ai-risk-management-framework

- Federal Reserve. Small Business Credit Survey. https://www.fedsmallbusiness.org/survey

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Brittany McMillen

Brittany McMillen

Brittany McMillen

Brittany McMillen